How Much Was Belle Burden's Husband in "Strangers" Actually Earning?

Hedge Funds vs. Big Law Pay

Everyone’s talking about Belle Burden’s Strangers: a Vanderbilt heiress’s account of her divorce from her hedge fund husband. It’s become a global cultural phenomenon.

Spotify invited us to their investor day last week, and the “Strangers” cover was on nearly every audiobook slide. Netflix just won the film rights in a six-way bidding war, with Gwyneth Paltrow set to play Belle herself. Burden has also done the full podcast circuit, ranging from Oprah to Call Her Daddy to SmartLess (may we add, Belle, we’d love to have you on The Wall Street Skinny!).

Therefore last week, after one of the most powerful women on Wall Street asked us to weigh in, we recorded our initial reactions. We analyzed the terms of the prenup Belle and her husband “James” signed, and explained why it felt wildly unfair that she wasn’t entitled to any of his earnings during their marriage. Ironically, one of my knee-jerk reactions — that she’d helped catapult him into another earnings echelon — turned out to be wrong. More on that later.

The whole time I was reading, I kept waiting for the Gone Girl second half — the part where you finally hear the other spouse’s account of the story. Without his firsthand narrative, we can’t know James’s exact version of events.

But there’s one picture the book never fully paints that we think we can: the financial one.

We know how the firms he worked for — hedge funds and how Arden, the fund of funds Belle’s uncle founded, where her husband was second in command — made their money. We know how these funds compensate people. From that, we can estimate what James earned over his career. Moreover, we also know firsthand what living in NYC with a family looks like; I had three kids in NYC while married to a man who worked in a very similar role to James’. And those numbers recast several of her “surprising” anecdotes from the book in a very different light.

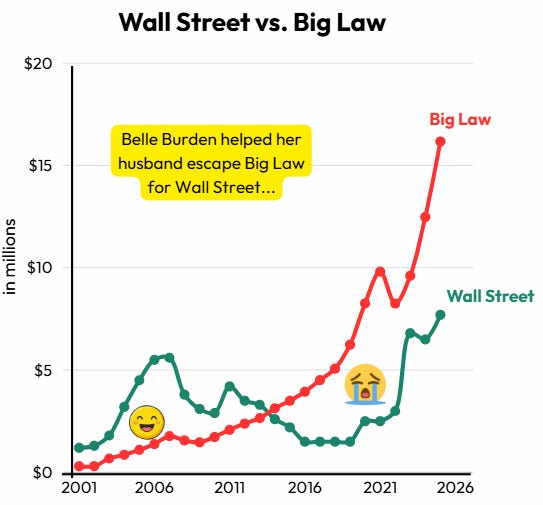

So we sat down to answer one question: “how much did Belle really juice her husband’s career?” My initial thesis was: look how much this Vanderbilt heiress helped her husband, pulling him out of Big Law and catapulting him onto Wall Street — the buy side, no less — and this is how he thanks her? After all, Belle is a woman with generational wealth who used her connections to upgrade her husband’s career from big law to high finance in the early 2000s. Let’s quantify that contribution, plus, it could give us a window into his mental state throughout the marriage (and its dissolution).

Shockingly, we ended up somewhere else entirely — a deep dive into the mechanics of how Big Law and hedge funds pay their people, and an understanding of how that calculus has completely flipped over the past two decades.

Ultimately, what started as a deep dive into the finances of a hedge funder became the story of how Big Law salaries have EXPLODED over the past decade.

Before we get too far in, a few notes:

Like the book, we’ll keep calling Belle’s husband “James” for simplicity’s sake.

As much as this is an attempt to reconstruct their finances to understand his “side of the story”, it’s also a glimpse into how the compensation structure works in finance vs. Big Law and how that’s changed with time.

There’s a saying, “all models are wrong, some are useful”. The chances we calculated EXACTLY what he was earning are virtually zero — but the trends are likely correct.

You could easily argue that Belle gave up her own “Big Law” earnings to be a stay-at-home wife and mother. Then again, the way she writes about hating corporate law makes us doubt she’d have stuck it out at Davis Polk long enough to make partner. Either way, her situation captures the real opportunity cost borne by highly successful women who step back from their careers for family. And it’s exactly why the prenup troubled us so much; under its terms, the spouse who stayed home with the children sacrifices a tremendous amount, yet there’s no financial acknowledgment of their incredibly demanding work. You can watch that discussion HERE.

So with that, let’s dive in.

Primer on Wall Street and Buyside Compensation

On Wall Street, you are paid with a base salary plus a bonus — the performance-based portion of your compensation.

For someone senior whose all-in comp lands in the $1–2 million range, your base salary can be as “low” as $200k, with the majority paid out as a year-end bonus. That structure gives the firm discretion to move comp up or down depending on how the year went.

If you’re senior at an asset management firm, though, you might also get a cut of the firm’s profitability. At private equity firms, this is called “carry“; in the hedge fund and asset management world, it’s called “points.” Points entitle an employee to a percentage of the firm’s profits according to a set formula. For example, 1 point = 1% of the profits.

This is why quantifying what James earned is a function of how much money the firms he was working at were taking in. It becomes an exercise in determining how much those firms held in assets under management (”AUM”), what they charged in fees, and how many points he was given over time.

Fees are generally split into two buckets: management fees and performance fees. A hedge fund might charge “2 and 20” — 2% of AUM plus 20% of any profits. But the rate depends on the strategy. The higher-risk, skill-intensive strategies — like “equity long/short”, macro, and relative value strategies — command those premium fees. Heck, some funds like Citadel and Balyasny (the so-called “multi-strategy” hedge funds) employ a pass-through model that charges even more. And the highest-fee hedge fund of all is RenTech, which charges 5 and 44 (!!), although to be clear: they aren’t open to the public and only employees of the firm can invest. Their Medallion fund is also the most successful hedge fund of all time with gross annual returns of 66% since 1988 (net returns of 39%).

“Long-only” strategies, by contrast, charge far less these days. Think 50–75 basis points (0.50%–0.75%), often with upside (like 20%) only if they beat a benchmark like the S&P500 or NASDAQ. And then you have fund of funds (which we’ll discuss), which have moved almost entirely to a flat-fee, consulting-based business.

Next, there are performance fees.

On top of their management fee, a hedge fund (and the old fund of funds model) takes a cut of the upside. 20% was the old hedge fund standard, though those fees have come down a tad. The mechanics are simple: if you invest $100mm and the fund grows it to $150mm, a 20% performance fee applies to the $50mm gain — so the fund keeps $10mm.

Therefore, approximating what James earned across his career hinges on four things:

(a) each firm’s AUM, (b) its fees, (c) its performance, and (d) his points.

There’s one more thing that is lost on most readers. “Working at a hedge fund” isn’t a single job. An administrative assistant can truthfully say they “work at a hedge fund,” and their pay will look nothing like a portfolio manager’s — the risk-taker who actually puts capital to work.

James, from what we can tell, landed on the business development side, not the investing side. That can still be lucrative when you’re earning points and sharing in the profits. But it isn’t where the eye-popping numbers live. You’re not pulling the $100 million packages that top traders command at the big multi-strategy funds like Citadel, Millennium, and Point72.

Here’s what’s wild, though. Those packages, once reserved for the elite risk-takers at the “pod shops”, have started migrating into corporate law. Which is exactly why, when we sat down to quantify how much Belle “helped” by pulling James out of Big Law and into high finance, we found something surprising. While in the early years it definitely helped his earning potential, in the long run, it likely hurt.

Big Law Compensation

Being a partner in Big Law has always been lucrative. What’s changed, and changed dramatically in the last 15 years, is how that pay stacks up against Wall Street.

For decades, practitioners in high finance looked down on lawyers as the help: the service providers who papered the deals while the real money got made on the other side of the table. For example, take the way “Leveraged Sellout,” a satirical blog written in 2006, painted the way an investment banker viewed their corporate law counterpart:

It’s on nights like tonight that I realize things could have been a lot worse…I realize that as tough as work is, I could have definitely ended up in much a shittier situation. For example, I could have been a Corporate Lawyer…

…Poor Andy. He used to want to run a hedge fund, now all he can hope for is to be In-House Counsel. He used to want to deck himself out in the cutting edge finely tailored business apparel, but now he’s bound for a closet full of golf shirts and tassel-y shoes. Andy used to want to be in the heat of things, sealing deals and wooing clients, but now he’s destined to be support staff.

Holla back, office?

— Leveraged Sellout, “BigLaw, BigSchmaw” (August 2006), leveragedsellout.com

The irony is, today our friend “Andy” here is likely laughing all the way to the bank.

First, let’s talk associate pay.

Continue reading this post for free, courtesy of The Wall Street Skinny.

| A guest post by

|

| A guest post by

|